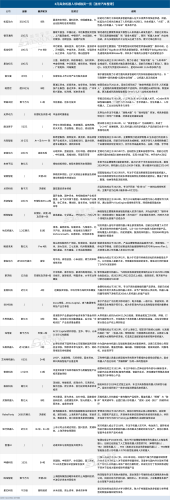

Gasgoo Munich- Capital is not slowing investments in embodied robotics in 2026 — if anything, it is accelerating. The sector is seeing an even more aggressive push for positioning.According to Gasgoo Automotive, March alone saw over 35 disclosed financing deals in embodied robotics and core components — a further uptick from February. Across the first quarter, more than 80 funding rounds were announced for robot bodies and key parts.Zoom out to the entire supply chain, and the numbers are even more staggering: Since the start of 2026, China's embodied AI sector has logged over 200 equity financing events. That's pulled in more than 30 billion yuan in total, averaging roughly 330 million yuan per day.Both the volume of deals and the scale of capital have hit record highs.Massive Rounds Surge to New Monthly HighsTrends this year show a clear concentration of capital at the top. The frequent appearance of billion-yuan rounds is the most direct proof.Gasgoo's data shows eight companies in the embodied robotics space disclosed rounds exceeding 1 billion yuan in March: Songyan Dynamics, Galaxy General, Jiajing Vision, StarMoment, Pasiini, Guanglun Intelligence, Lingchu Intelligence, and Zhijian Dynamics.Including the first two months, the sector saw 16 billion-yuan rounds in Q1. February accounted for six — from LimX Dynamics, Lingxin, Xinghai Map, Zhipingfang, Qianxun Intelligence, and Anhui Shenji — while January saw two, from BrainCo and Zibianliang. Consequently, February and March each drew in over 10 billion yuan.By comparison, all of 2025 saw just six deals of similar size.This means 1 billion yuan has become the hard threshold for top-tier projects and the entry ticket to the first league. It also highlights the intense competition to secure leading projects.Image Credit: Galaxy GeneralSpecifically, March's largest round went to Galaxy General at 2.5 billion yuan. Combined with the $300 million raised in late 2025, the company has secured nearly 5 billion yuan in just three months — a clear sign of the heat. Meanwhile, Lingchu Intelligence and Zhijian Dynamics each closed 2 billion yuan rounds in March.But here's what stands out: unlike previous mega-rounds that typically arrived at Series B or later, several of March's eight billion-yuan deals — including Guanglun Intelligence, Lingchu Intelligence, and Zhijian Dynamics — were secured at the Series A stage.In traditional venture logic, Series A is for proving technical feasibility, typically raising tens of millions. The frequency of mega-rounds at this stage in embodied AI suggests the starting line for competition is being pushed forward. Serious competition used to begin at Series B; now, companies need to be fully prepared by Series A.One reason is the inherently high costs and long cycles of embodied robotics.As complex systems fusing AI, precision manufacturing, sensors, chips, and materials, embodied robots require massive capital at every stage — from core algorithms and key components to prototyping and mass production.Take UBTECH: in 2025 alone, it poured over 500 million yuan into R&D — 25.6% of revenue — with more than 270 million yuan dedicated to full-size humanoid robots. Over the past five years, UBTECH's R&D spending totaled nearly 2.5 billion yuan, while sales expenses exceeded 2 billion yuan.As embodied AI accelerates into commercial validation, mass production has become the core challenge. Companies are forced to invest heavily earlier to tackle supply chains, production lines, delivery, and after-sales — directly driving up the capital requirements for Series A rounds.On the other hand, shifts in the investor base cannot be ignored.Unlike previous waves led by market VCs, this round has seen the National AI Industry Fund, China Development Bank Finance, and various local state-owned asset platforms enter aggressively. From the Beijing Robotics Industry Fund to Xi Venture Capital and Shenzhen Capital Group, governments are systematically positioning embodied AI as a core engine of regional "new quality productive forces."When the "national team" starts betting real money, valuation logic goes beyond simple discounted cash flow. It now includes premiums for supply chain security and regional competition — variables traditional models can't quantify.Of course, capital's "fear of missing out" is further intensifying the trend."Everyone knows there's a bubble, but do you dare sit it out? If you don't get in now, you might never catch up," one investor remarked. It captures the prevailing mindset: "Better to overpay than to miss out entirely."As capital intensity heats up, valuations for top-tier embodied robotics firms have surged.Image Credit: Xinghai MapMore than a dozen domestic players are now valued at over 10 billion yuan. Galaxy General, Xinghai Map, and Qianxun Intelligence have even surpassed the 20 billion yuan mark.Notably, as valuations at the top become prohibitively expensive — or simply inaccessible — some capital is shifting toward mid-tier or earlier-stage projects.Zhijian Dynamics, for instance, closed five rounds totaling 2 billion yuan in just six months, becoming the sector's youngest unicorn. Early-stage projects like Xinuo Future, Octopus Power, and RoboParty also secured 100-million-yuan rounds in their latest financing.This divergence also reflects the fact that technical roadmaps in embodied AI have yet to converge. Bipedal or wheeled? How to design joints? Configure sensors? There are no standard answers yet — which means plenty of room for new possibilities."In the large model space, we expect a startup to break out within the next two years. We're keeping a close eye on small teams spinning out of giants like ByteDance — they often have strong technical depth, iterate fast, and make decisions flexibly," an executive at a leading firm said.Viewed this way, the rush into early-stage projects is essentially a diversified investment strategy to hedge against that uncertainty.While this "broad investment approach" has given many early projects the seed capital needed to survive and explore — injecting vitality and validating diverse paths — it has also fueled froth. Some early-stage projects, lacking core technical moats or clear business models, are securing high valuations based solely on packaging and team pedigree.It's why some investors bluntly admit that even among today's 10-billion-yuan unicorns, some will eventually fail.That's not alarmism. There are two types of high-valuation companies today. One has proven itself with revenue and profit — Unitree, for example. Its 2025 revenue hit 1.708 billion yuan with a net profit of 600 million yuan, a margin of roughly 35%. That's standout performance in any sector.Even so, Unitree's IPO valuation implies a price-to-sales ratio of about 25 times (with a 10% float, its initial market cap reaches 42 billion yuan). Even factoring in a growth premium, one has to ask: has the sector's valuation level already overdrafted expectations for years to come?The other type comprises companies that have yet to close the commercial loop but secured 10-billion-yuan valuations based on technical roadmaps and team backgrounds. Whether they can deliver results matching those valuations before the capital tide recedes remains to be seen.After all, raising money and turning it into a sustainable business are two very different things.Monetization Begins, But the Scale Test Is Just StartingWhile most players in embodied robotics still rely on funding to survive, a few have initially closed the "product-delivery-revenue" loop and kicked off large-scale deliveries.UBTECH recently released its 2025 earnings report. Total revenue last year reached 2.001 billion yuan, up 53.3% year-over-year. Net loss narrowed by 31.9% to 790 million yuan, while adjusted net loss — excluding share-based payments — narrowed 24.5% to 691 million yuan.Revenue from full-size humanoid robots and solutions surged from 35.6 million yuan in 2024 to 821 million yuan — a 2203.7% spike. Its share of total revenue leapt from 2.7% to 41.1%, making it the company's largest revenue stream.Image Credit: UBTECHCorrespondingly, sales of full-size humanoids hit 1,079 units in 2025, a staggering 35,866.7% increase. Behind this growth, its Walker S series — focused on handling, sorting, and quality inspection — has been deployed in industrial settings like automotive manufacturing, 3C electronics, and new energy battery production.Unitree also delivered solid growth in 2025, with revenue reaching 1.708 billion yuan, a 335% jump, and net profit hitting 600 million yuan, up 674%.It's worth noting, however, that Unitree's R&D spending was still under 100 million yuan in 2025. Moreover, 70% of its humanoid robots were sold to universities and research institutions, meaning the commercial loop is still in the early stages of transitioning from research to industry.Behind these figures, humanoid robots are fast becoming Unitree's main revenue driver.Since launching the full-size H1 in August 2023, humanoid revenue reached 2.967 million yuan in 2023, 107 million yuan in 2024, and 595 million yuan in the first three quarters of 2025. That represents 1.88%, 27.60%, and 51.53% of total revenue respectively. In 2025, thanks to shipments exceeding 5,500 units, revenue from humanoids successfully overtook that of quadruped robots.Dobot, after pivoting from "collaborative robot leader" to a "full-form embodied AI platform," generated about 20 million yuan in embodied robotics revenue in 2025 — up 418.8%. This was driven by products like the humanoid Dobot Atom, wheeled humanoid Dobot ATOM-W, and quadruped Rover X1.These figures indicate that embodied robotics is accelerating its shift from R&D to commercial deployment.At the same time, a sober reality check is in order: while leaders have proven their revenue models, the broader industry remains in the red or barely profitable. The leap from delivery to profitability, and from research labs to industrial scale, remains the biggest test for 2026.Rapid mass production by robot makers is boosting upstream component suppliers, who are racing to build a "second growth curve" through embodied AI.Recently, supply chain players like Black Sesame, RoboSense, and Tuopu Group all highlighted the significant revenue boost from embodied AI in their 2025 earnings reports.Image Credit: Black SesameBlack Sesame's embodied AI solutions generated 96.3 million yuan in 2025. While that's far smaller than its autonomous driving business, the gross margin hit 48.7% — nearly 10 percentage points higher — helping push the company's overall margin above 40%.As a core perception supplier, RoboSense sold 303,000 LiDAR units for robots in 2025, a 1141.8% surge, covering applications from mowing and delivery to humanoids. Consequently, robot business revenue reached 709 million yuan, up 257.7%, with a gross margin of 39.7% — significantly higher than the 19.1% margin in its ADAS business.Tuopu Group broke out its robot actuator business for the first time in its 2025 report. Revenue came to 13.59 million yuan. While modest in scale, the segment boasted a 28.25% gross margin, notably higher than the 18.04% margin for auto parts.Behind these numbers, Black Sesame, RoboSense, Tuopu, and others are transferring their automotive expertise — R&D, precision manufacturing, cost control, mass delivery, and client resources — into the robot sector. They're aiming for synergy between smart car components and robot components to build that new growth curve.This is the core logic and fundamental advantage for almost every auto supplier crossing into embodied robotics. Large-scale manufacturing and cost control are widely seen as the biggest "key advantages" for Tier 1 automakers making the leap.However, while the advantages for auto suppliers are clear, not everyone is bullish on the crossover.Many automakers are now building their own robots. But an executive at a leading embodied AI firm argues that while OEMs have significant capital and manufacturing muscle, these aren't insurmountable moats. Startups can catch up quickly by poaching teams and outsourcing manufacturing — a process accelerated by the flood of capital.Even autonomous driving, often seen as a sibling technology, differs fundamentally in its Vision-Language-Action (VLA) models. Driving solves a "perception-decision-control" loop, whereas robots must grapple with physical interaction and dexterity — challenges where experience doesn't directly transfer.Instead, the iteration speed and flexibility of startups are hard for many automakers to match.Image Credit: Lens TechnologyThen there's Lens Technology. As a full-stack "platform" player, its robotics business moved into large-scale delivery in 2025. Shipments of humanoids and quadrupeds both exceeded 10,000 units, with robotics revenue surpassing 1 billion yuan.Behind these numbers lies a reality: massive volumes of components are being assembled into robots, and swarms of embodied machines are moving from labs into real-world applications — taking on specific tasks in manufacturing, logistics, and home services.Looking ahead to 2026, consensus forecasts suggest humanoid robot shipments alone could jump from just over 10,000 units in 2025 to tens of thousands.So, if the pre-2026 era was defined by fundraising, technical roadmaps, and team pedigree, the post-2026 era will shift the battleground to supply chain management, cost control, and customer service. Crucially, customer retention and willingness to reorder will largely determine whether companies can establish a foothold and sustain growth.ConclusionMassive rounds, ten-billion-yuan valuations, deliveries in the tens of thousands — these numbers sketch the hype and intensity of the embodied AI sector in 2026.Yet foam and value are two sides of the same coin. Capital has accelerated the industry's maturation with real money, but it has also inflated a valuation bubble. UBTECH, Unitree, and others have proven the viability of their business models with real orders, raising the market's expectations across the board.When market enthusiasm cools, the survivors won't necessarily be those with the highest valuations or the biggest funding rounds. They will be the companies that can turn technology into product, product into service, and service into sustainable cash flow.