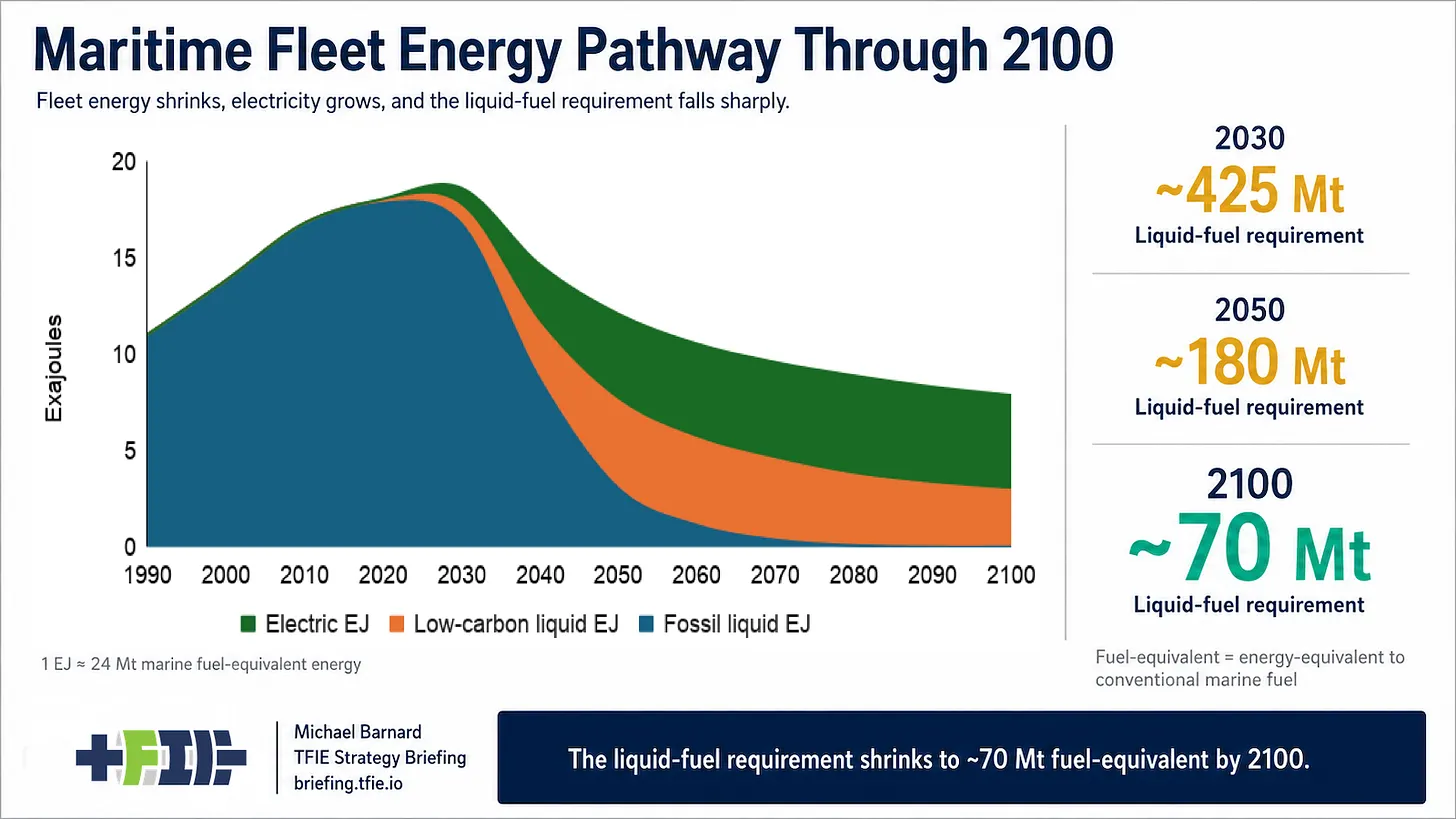

Maritime fuel debates usually start with the wrong object. They look at today’s bunker fuel demand, line up replacement molecules, and ask whether ammonia, methanol, hydrogen, LNG, biofuels, or synthetic fuels can scale far enough to replace it. That sounds like a practical question, but it skips the larger one: how much maritime fuel demand remains after the energy transition changes the cargoes that ships carry. The important result from my rebaselined maritime energy pathway is that fossil fuel cargo is not just large by mass. It is disproportionately important to shipping energy. Fossil fuels are roughly 40% of maritime tonnage, but in the model they represent about half of maritime freight energy because coal, oil, and gas are mostly long-haul bulk trades. Moving a ton of scrap metal a short distance and moving a ton of oil or LNG across oceans are not the same transport-energy problem, even if both show up as one ton in a cargo table. That distinction matters because shipping fuel demand is driven by transport work, not just tons loaded at ports. Ton-kilometres are the better mental model. Fossil fuel cargoes travel long distances in very large flows, so their decline removes more than a proportional share of cargo mass. It removes a larger share of the ocean work and the fuel burned to do that work. This is the part that fuel-first narratives tend to miss. In a serious energy transition, coal demand falls, oil demand falls, and gas demand falls. That means fewer bulk carriers and tankers moving fossil energy around the world. The maritime sector does not have to find a one-for-one replacement fuel for all of that work, because a material share of the work should disappear. Raw iron ore is the adjacent exposed category. It is not part of the 40% fossil-fuel tonnage number, but it is another large, long-haul bulk trade tied to the old industrial geography. As China’s construction pulse slows, steel demand shifts, scrap use rises, electric arc furnaces take more share, and more iron reduction can occur closer to renewables-rich mining regions, raw iron ore shipping is unlikely to behave like a permanently rising global constant. That does not make iron ore shipping vanish, but it does make it a poor basis for assuming today’s bulk-shipping energy demand simply continues. Other parts of shipping grow in the transition, but many of them are better suited to electrification than the fossil-bulk trades they partially replace. Offshore wind construction and service vessels grow. Ferries and short-sea routes expand where road congestion, urban growth, islands, ports, and regional logistics justify them. Inland and coastal freight can grow as supply chains reorganize and ports electrify. These are not all battery-only segments, but they tend to have more regular routes, shorter distances, known terminals, and better opportunities for charging, shore power, and battery-dominant hybrid operation than long-haul coal, oil, gas, and raw iron ore trades. The result is a very different maritime fuel problem. A one-for-one substitution model makes the alternative-fuel task look enormous, and it is enormous if the goal is to preserve today’s oil-shaped marine energy system with different molecules. A denominator-first model asks what fuel-burning work is left after fossil cargo declines, raw iron ore exposure is included, electrifiable segments grow, short routes electrify, and efficiency trims the remaining fleet. That is where batteries enter the picture without pretending to be magic. Inland shipping, ferries, harbor craft, many short-sea routes, and some coastal services are structurally suited to batteries, shore power, terminal charging, and battery-dominant hybrid operation. Recent work in Nature Energy on short-sea electrification found a surprisingly large eligible wedge of maritime energy once route structure, battery size, ship classes, and operating patterns are tested rather than waved away. Those ships do not need a universal global molecule. They need electricity, charging infrastructure, operational planning, and procurement discipline, which is less glamorous than a new global fuel chain and usually more useful. Operational efficiency also matters, but it belongs in the same denominator logic. Slow steaming, routing, hull management, propeller improvements, wind assistance where it fits, hybridization, and better logistics all reduce fuel demand in the part of the fleet that still burns fuel. None of them turns a large oceangoing vessel into a battery ferry, and none of them avoids the need for residual liquid fuels. They reduce the size of the problem those fuels have to solve. Only after those reductions does the residual fuel debate become useful. Biomethanol, biodiesel, hydrotreated vegetable oil, and potentially ethanol belong in the conversation for vessels and routes that still need liquid fuels and where feedstock, lifecycle emissions, bunkering, safety, and cost make sense. They do not have to replace today’s entire marine fuel pool to matter. They have to serve the smaller pool of voyages that still need energy-dense liquids after cargo, route, and efficiency changes have done their work. In that context, hybrid ships make alcohol fuels range extenders, not rivals to electrification. That is one reason ammonia and hydrogen remain weak centerpieces for shipping decarbonization. They ask the sector to build expensive new fuel chains around molecules with major cost, safety, energy-density, handling, and lifecycle-accounting problems, often while ignoring the shrinking denominator. Synthetic fuels have their own very long electricity and conversion-loss stack. LNG remains mostly a fossil incumbent strategy with a different label and a methane problem it has never convincingly escaped. The policy discussion is slowly moving toward better accounting, especially with well-to-wake emissions and tighter International Maritime Organization targets, but targets do not create viable fuel pathways by themselves. Alternative-fuel capability on a ship order is not delivered decarbonization. A pilot bunkering event is not fleet transformation. The useful evidence comes later: operating routes, delivered fuel, verified lifecycle emissions, repeat procurement, and economics that survive outside demonstration conditions. The public reading of the pathway is straightforward. Count fuel only where ships remain fuel-burning. Discount the parts of shipping where cargo disappears, where batteries and shore power are advantaged, and where operational changes reduce energy use. Then argue about residual liquids for the work that remains, not for the entire legacy bunker-fuel pool. That is also how maritime fuel economics should be compared: by useful work and residual demand, not by preserving today’s fuel pool and asking every molecule to fill it. Shipping is not going to decarbonize by finding one universal alternative fuel and applying it to the existing oil-shaped system. It has to recognize that some of today’s largest and most energy-intensive cargo flows are structurally exposed by the transition itself. When 40% of tonnage represents about half of freight energy, the first fuel transition is not a molecule. It is the disappearance of a lot of long-haul fossil work. A longer maintained version of this analysis is available at TFIE Strategy Briefing: Shipping’s Fuel Transition Starts With Less Fuel, Not Better Molecules It is part of Michael Barnard’s broader work on maritime decarbonization, shipping fuel pathways, electrification, residual liquids and 2100 transition scenarios.